The battle for global supremacy is in full swing with the US, the leader of the free world on one side and China, a rising power on the other side. This battle is playing out in the economic arena, the military arena and the tech arena. At the end of 2022, the Biden administration imposed a sweeping set of export controls that included measures to cut China off from certain semiconductor chips and chip-making equipment. Whilst Donald Trump started the trade war with China President Biden has now not just continued but expanded the trade war by banning access to advanced Chips for China. The American ban brings into sharp focus the importance of Semiconductors and the battle to control this critical technology.

What are Semiconductors?

Generally, semiconductor refers to a material – like silicon – that can conduct electricity much better than an insulator such as glass, but not as well as metals like copper or aluminium. Semiconductor chips are typically made from thin slices of silicon, that are the size of one’s hand and thinner than a piece of human hair. They have complex components laid out on them in specific patterns. These patterns control the flow of current using electrical switches – called transistors. Like we control an electrical current in our home by flipping a switch to turn on a light a semiconductor switch is entirely electrical, with – no mechanical components to flip. These chips contain tens of billions of switches in an area not much larger than the size of a fingernail.

From the earliest days of the missile race, the Pentagon was fixated on applying computing power to defence systems. The first major application of chips was in missile guidance systems. Among the earliest commercial applications for semiconductor chips were pocket calculators, which became widely available in the 1970s. These early chips contained a few thousand transistors. In 1989 Intel introduced the first semiconductor to exceed a million transistors on a single chip. Today the global market for semiconductors is driven by growing demand for smartphones, tablets, digital TVs, wireless communications infrastructure, network hardware and all other goods that use computers.

Today, the largest chips contain more than 50 billion transistors. This trend is described by Moore’s law, which says that the number of transistors on a chip will double approximately every 18 months. Today semiconductors are tiny electronic switches that run computations inside any and all computers.

The Chip Supply Chain

Manufacturing semiconductors is a highly complex and immensely precise process with other 300 stages. These include raw wafers, commodity chemicals, specialty chemicals, and bulk gases; all are processed and analysed by upwards of 50 different types of processing and testing tools. Those tools and materials are sourced from around the world and are typically highly engineered. Further, most of the equipment used in semiconductor manufacturing, such as lithography and metrology machines, rely on complex supply chains that are also highly optimized, and incorporate hundreds of different companies delivering modules, lasers, mechatronics, control chips, optics, power supplies, and more.

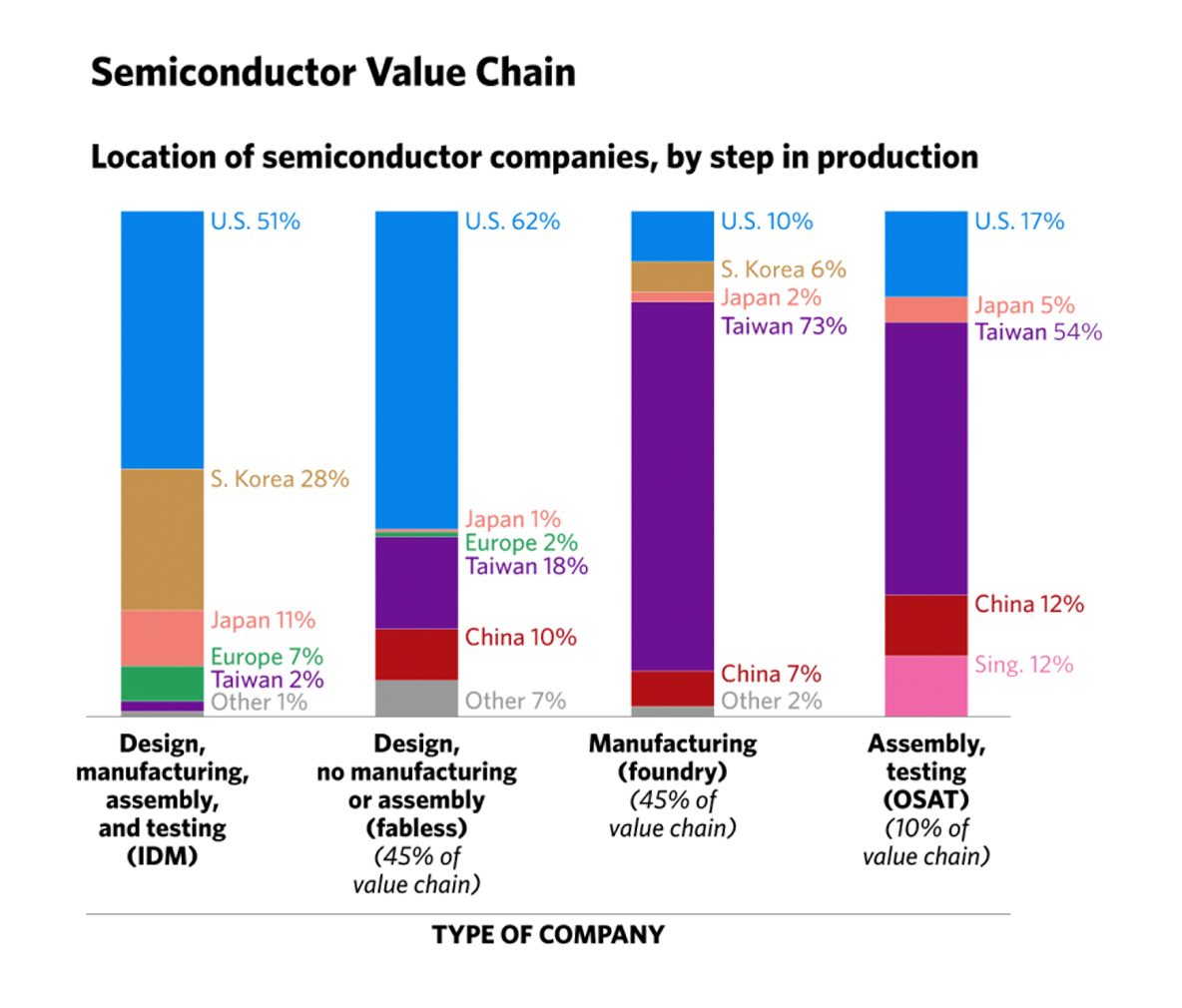

The production chain for semiconductors does however have three distinct components, this is design, which constitutes 45% of the value chain. Then fabrication which constitutes another 45% of the value chain. And then assembly, testing and packaging, which constitute 10% of the value chain.

Two groups of companies dominate the design aspect, these are integrated device manufacturers, which have integrated design with production capabilities and therefore have in-house technology to produce semiconductors. Then there are fabless firms, which focus only on chip design and partner with a contract foundry like Taiwan Semiconductor Manufacturing Co (TMSC) to manufacture them. TSMC beginning in 1987 pioneered the “pure-play foundry” model that focused solely on manufacturing other companies’ Chip designs. Eventually they established integrated device manufacturers like Intel, as well as AMD and Qualcomm sold off their own foundries, finding it more profitable to contract production out to TSMC and its only comparable competitor, South Korea’s Samsung. This sparked a boom in innovation and specialisation as fabless chip designers could channel all their resources into pushing the boundaries in niches ignored by the likes of Intel, which focused mostly on general purpose processors. Building cutting edge factories that manufacture semiconductors costs more than $20 billion. It’s also become increasingly technologically sophisticated, requiring expensive, highly specialized materials and tools that themselves are made by a very small number of companies. As a result, TSMC controls more than 50% of the global semiconductor foundries, whilst Taiwan an as a whole possesses 75% of the worlds fabless foundries.

This sparked a boom in innovation and specialisation as fabless chip designers could channel all their resources into pushing the boundaries in niches ignored by the likes of Intel, which focused mostly on general purpose processors. Building cutting edge factories that manufacture semiconductors costs more than $20 billion. It’s also become increasingly technologically sophisticated, requiring expensive, highly specialized materials and tools that themselves are made by a very small number of companies. As a result, TSMC controls more than 50% of the global semiconductor foundries, whilst Taiwan an as a whole possesses 75% of the worlds fabless foundries.

Taiwan and the handful of fabless facilities around the world they all rely on equipment, tools and software produced by external firms to make semiconductors. TSMC, like other foundries, is dependent on other companies to supply the equipment needed for production. But only a small number of manufacturers produce this equipment: Five companies account for more than 75% of global supply. Three of these companies are based in the US – Applied Materials, Lam Research Corp. and KLA Corp. – and the other two are Japanese firm Tokyo Electron and Dutch company ASML. Production at advanced levels requires huge investments and access to complex global supply chains producing chemicals at high levels of purity and lenses, mirrors, valves and tubes engineered to the highest levels of precision. It also requires access to sophisticated electronic design automation tools and deep or extreme ultraviolet lithography tools. Both are dependent on US Intellectual Property. Made in China

Made in China

Semiconductors represents a rare area in which the Chinese economy is dependent on the rest of the world—rather than the other way around. In 2015 China’s “Made in China 2025” strategy aimed to change this by vastly increasing domestic semiconductor production. One reason this had to change was because China spends $432 billion on imported microprocessors, equivalent to total expenditure on grain and crude oil imports.

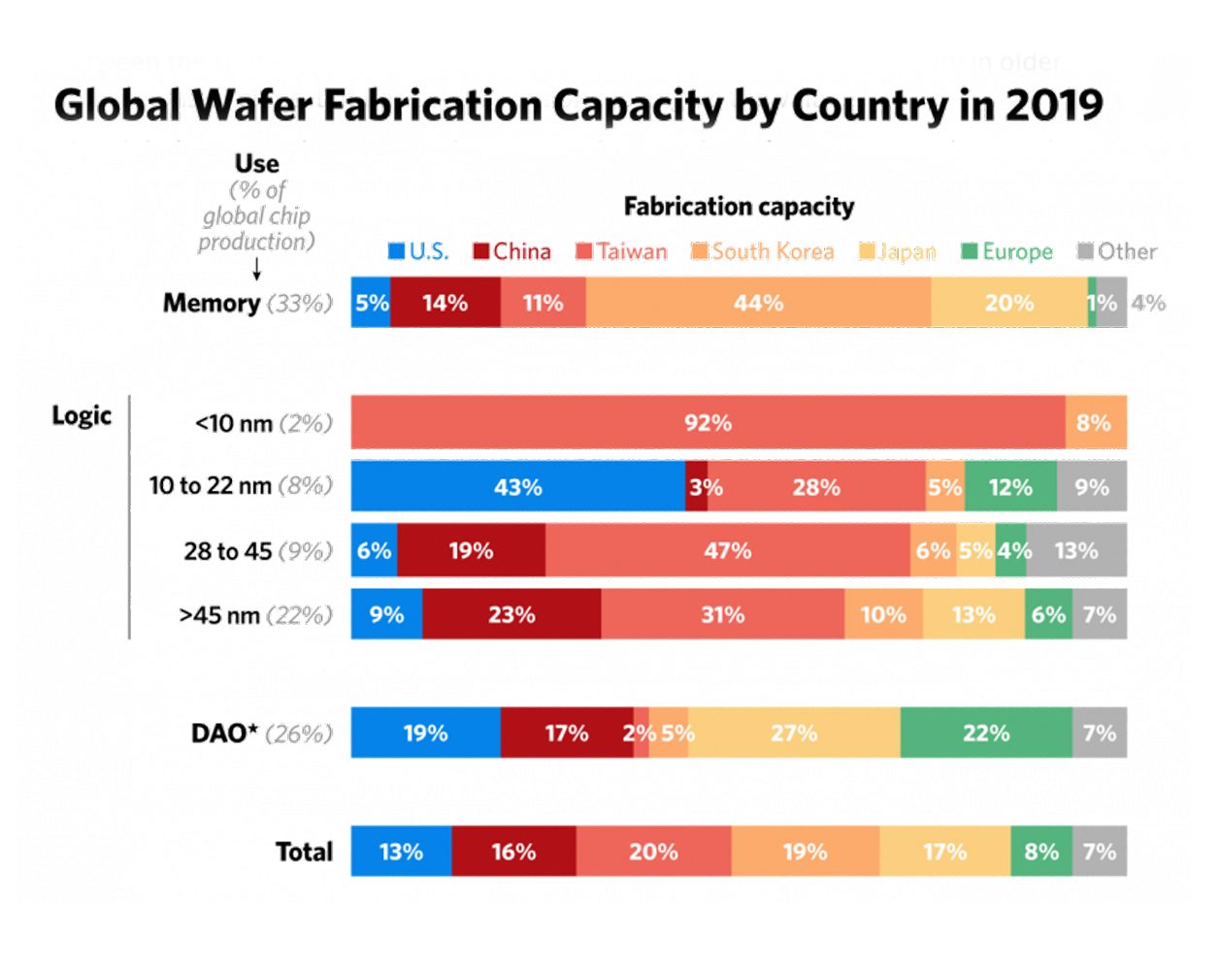

Prior to the last half-decade, China spent more than 30 years and tens of billions of dollars to build a domestic semiconductor industry, showering its national champions with resources to compete with Western companies. Despite these investments, Chinese semiconductor companies make up a relatively small part of the global market. Today China’s own microprocessor industry now manufactures significant quantities of microprocessors at the less advanced production nodes, i.e. 24 nanometers upwards (the nanometer is the measure of the gap between etched circuits on a silicon chip). But China is still a long way from being able to produce microprocessors at the most advanced production nodes, now 5 and soon to be 3 nanometers. The production of these advanced nodes is dominated by two corporations, Taiwan’s TSMC and South Korea’s Samsung.

Over the past decade, the Chinese government has doubled down on its efforts to develop and indigenise its semiconductor industry. This emphasis stems from a concern among Chinese leadership that she has been too reliant on foreign firms for access to advanced commercial semiconductors and semiconductor manufacturing equipment. China’s push for chip dominance has yielded some success in recent years; however, due to lack of access to critical intangible expertise, China is likely to remain behind the US and other US allies in this supply chain.

For the US, China’s tech rise possess a challenge that can’t be left to another day. Supercomputers, AI, robotics and the internet of things etc will all require advanced semiconductors and China possess a threat that the US is now moving to address. US export controls against China’s semiconductor industry will have real impact on China but it will likely lead to more aggressive Chinese retaliation. Given the dominance of US and Western-developed technology, US restrictions will severely disrupt China’s semiconductor industry, unless China can make its own breakthroughs.